RegTwin AI: Full Platform Blueprint

The first autonomous regulatory intelligence platform — monitor, predict, defend, simulate, report.

“Regulatory compliance will not be solved by workflow software. It requires autonomous intelligence that thinks like an examiner, responds like a specialist, and learns from every finding it has ever seen.”

Paper DNA

Domain

AI & Regulatory Compliance

Maturity

Blueprint

Market Size

~5,000 FDIC banks · $500K–$1M ARR each

Connected To

RegTwin AI closes the full regulatory loop — monitor → predict → defend → simulate → report — in a single modular platform no existing RegTech vendor offers end-to-end.

The Defend module alone addresses a $5M–$50M per-remediation-cycle pain point across ~5,000 FDIC-insured US banks, representing $500K–$2M ARR per institution at scale.

The platform's competitive moat is irreplicable: 20 years of examiner-facing intelligence encoded into AI agents that think like regulators, not workflow tools.

The Vision

The first autonomous regulatory intelligence platform that monitors what's coming, defends when it arrives, proves you did it right, and prepares you for what's next.

One platform. Five modules. One toggle to turn each on.

Every module in this platform was designed around a single insight: the most expensive moment in regulatory compliance is the moment you are surprised. Every MRA, every consent order, every examiner finding that catches a bank off guard represents a failure of anticipation — and anticipation is exactly what this platform provides.

The five modules are not independent products. They are a closed loop. Monitor feeds Predict. Predict pre-loads Defend. Defend stress-tests through Simulate. Simulate validates Report. Every data point generated by one module makes the next module smarter.

Platform Architecture

┌─────────────────────────────────────────────────────────────┐

│ RegTwin AI Platform │

│ │

│ ┌─────────────────────────────────────────────────────────┐ │

│ │ Client Dashboard │ │

│ │ Module tabs render dynamically based on feature flags │ │

│ └─────────────────────────────────────────────────────────┘ │

│ │ │

│ ┌─────────┬──────────┬────┴────┬──────────┬──────────┐ │

│ │ Monitor │ Predict │ Defend │ Simulate │ Report │ │

│ │ Module │ Module │ Module │ Module │ Module │ │

│ └────┬────┴────┬─────┴────┬────┴────┬─────┴────┬─────┘ │

│ │ │ │ │ │ │

│ ┌────┴─────────┴──────────┴─────────┴──────────┴──────┐ │

│ │ Shared Agent Orchestrator │ │

│ │ (Routes tasks to specialized agents) │ │

│ └──────────────────────┬───────────────────────────────┘ │

│ │ │

│ ┌──────────────────────┴───────────────────────────────┐ │

│ │ Core Engine │ │

│ │ Auth & Tenants · Document Ingestion · Feature Flags │ │

│ │ Vector Store · Audit Trail · Reg Taxonomy · Billing │ │

│ └──────────────────────────────────────────────────────┘ │

└─────────────────────────────────────────────────────────────┘

The architecture enforces a single principle at every layer: no module should have to rediscover what another module already knows. The Shared Agent Orchestrator is the connective tissue — it routes tasks, shares context, and ensures the whole system gets smarter with every interaction.

Core Engine — The Foundation

Everything runs on this. Built once, shared by all five modules. The Core Engine is where trust is earned — with the bank, with the regulators, and with the AI system itself.

Auth & Tenant Management

- Multi-tenant architecture — each bank is an isolated tenant

- Role-based access: Admin, CCO, Compliance Analyst, Internal Audit, Read-Only

- SSO/SAML integration (banks require this — no negotiation)

- Tenant-level encryption keys — Bank A's data is never accessible from Bank B's queries

Document Ingestion Pipeline

- Accepts: PDF, DOCX, email (.eml), structured data (CSV, Excel)

- OCR for scanned regulatory letters — even paper-born findings get processed

- Auto-classification: Is this an MRA? A consent order? A policy update? An internal audit finding?

- Chunking and embedding into the vector store for AI retrieval

- Every document receives a unique ID, timestamp, and chain-of-custody log

Feature Flag System

{

"tenant_id": "bank_001",

"modules": {

"monitor": { "enabled": true, "tier": "standard" },

"predict": { "enabled": true, "tier": "standard" },

"defend": { "enabled": true, "tier": "premium" },

"simulate": { "enabled": false, "tier": "enterprise" },

"report": { "enabled": true, "tier": "standard" }

}

}

One config change. The module appears in their dashboard. The invoice updates. This is how the platform lands and expands without a new sales cycle for each feature.

Regulatory Taxonomy

A master knowledge graph of every major US regulator — OCC, Fed, CFPB, FDIC, SEC, FINRA, and state regulators — mapped to examination types, finding categories, control domains, and evidence standards. This taxonomy is what allows the AI to understand context, not just content.

Vector Store & Knowledge Base

The long-term memory of the platform. Stores embedded versions of all ingested documents, plus the encoded domain expertise — examiner expectations, response patterns, control frameworks — that makes the AI's judgement valuable rather than generic.

Audit Trail

Every AI action is logged: which agent ran, what input it received, what output it produced, what confidence score it assigned. The log is immutable. Regulators can inspect exactly how any recommendation was generated. This is not optional architecture — it is the product.

Billing & Usage Tracking

Per-module metering, usage tiers, and Stripe-integrated billing automation. Transparency in consumption builds trust and removes friction from the upsell conversation.

Module 1: Monitor

Purpose: Continuous surveillance of the regulatory landscape. Tells the bank what's coming before it arrives.

Agents

| Agent | Role |

|---|---|

| Regulatory Scanner | Crawls regulator websites, the Federal Register, enforcement actions, and guidance updates. Identifies changes relevant to the tenant's specific profile. |

| Impact Assessor | Takes each regulatory change and maps it to the bank's control environment. Answers: "Does this affect us? How severely? Which business lines?" |

| Alert Composer | Generates human-readable alerts with severity ratings, affected business lines, and recommended actions — calibrated to the reader's role. |

Key Workflows

- Daily Scan — Automated sweep of regulatory sources; new items flagged and classified

- Impact Analysis — Each flagged item assessed against the tenant's profile and control inventory

- Alert Distribution — Relevant stakeholders notified based on business line and access role

- Trend Tracking — Aggregates regulatory direction over time: "The OCC is increasing focus on model risk this quarter"

What Monitor Produces

- Daily and weekly regulatory digests

- Impact assessments with severity scores

- Trend analysis dashboards

- A continuous feed into the Predict module — regulatory trends become examination predictions

Module 2: Predict

Purpose: Anticipate examination findings before the examiner arrives. Surface control gaps proactively.

The core insight behind Predict: every regulatory finding that has ever been issued publicly is a training signal. Patterns exist across the industry that individual banks cannot see from inside their own institutions. Predict sees all of it.

Agents

| Agent | Role |

|---|---|

| Pattern Analyst | Analyzes historical enforcement actions, consent orders, and MRAs across the industry. Surfaces patterns: "Banks of your size and charter type are being cited for X." |

| Control Gap Detector | Compares the bank's control inventory against current regulatory expectations. Finds the gaps before an examiner does. |

| Risk Scorer | Assigns probability scores to potential findings. Answers: "What are the top 5 things an OCC examiner would flag if they walked in today?" |

| Early Warning Composer | Generates actionable reports with specific, prioritized remediation suggestions. |

Key Workflows

- Peer Analysis — "Here's what banks like yours are being cited for" — based on public enforcement data, anonymized and aggregated

- Control Health Check — Automated gap analysis against current regulatory expectations

- Examination Readiness Score — A single 1–100 metric with full drill-down capability

- Proactive Remediation — "Fix these 3 things before the examiner notices" — ranked by probability and severity

What Predict Produces

- Examination readiness score

- Risk areas ranked by probability and severity

- Control gap reports

- Proactive remediation recommendations

- Pre-loaded context for the Defend module — predicted findings become draft response templates

Module 3: Defend — The Revenue Driver

Purpose: When a finding lands, decompose it, map it, plan the response, draft the letter, and package the evidence. End to end.

This is where the platform's value is most immediate and most quantifiable. A single MRA remediation cycle costs a bank $5M–$50M in consultant time. Defend compresses that cycle by 60% — and improves first-pass acceptance rates.

Agents

| Agent | Role |

|---|---|

| Finding Decomposer | Takes a regulatory finding — MRA, consent order, examination comment — and breaks it into atomic obligations. Each obligation is tagged: control domain, severity, evidence type required, deadline. |

| Control Mapper | Maps each obligation to the bank's existing control inventory. Identifies: which controls already address this, which partially address it, where the gaps are. |

| Remediation Planner | For each gap, generates a remediation plan with milestones, suggested owners, evidence checklists, and timeline dependencies. Powered by 20 years of PMO methodology. |

| Response Drafter | Drafts the formal response letter. Calibrated to the specific regulator's expectations — OCC vs Fed vs CFPB have fundamentally different styles, and the AI knows the difference. |

| Evidence Tracker | Manages evidence collection. Assigns tasks to owners, tracks completion, validates that evidence actually satisfies the obligation, flags gaps for follow-up. |

| Package Assembler | Compiles the final audit-ready submission: response letter, remediation plan, evidence appendix, control mapping, timeline commitments — structured for regulator review. |

Core Workflows

Finding Intake:

Upload finding document

→ OCR / parse

→ Auto-classify (MRA / consent order / informal comment / MRIA)

→ Finding Decomposer breaks into atomic obligations

→ Each obligation receives a unique ID and enters tracking

Response Generation:

For each obligation:

→ Control Mapper checks existing controls

→ Gaps identified and prioritized

→ Remediation Planner creates milestone plan

→ Response Drafter generates formal language

→ Human reviews and edits

→ Package Assembler compiles submission

Pre-Submission Stress Test:

Before submission:

→ AI reviews complete package as if it were the examiner

→ Flags weak spots: "An OCC examiner would push back here because..."

→ Suggests strengthening language or additional evidence

→ Confidence score: "This response has an 82% first-pass acceptance probability"

Response Drafting — The Differentiating Feature

This is where 20 years of examiner-facing experience becomes a product.

What the AI knows that competitors cannot replicate:

- OCC examiners want specificity on root cause. "We will enhance our processes" gets the letter returned. "We will implement automated daily reconciliation of Account Type X against Source System Y by Q3 2026, validated by an independent testing team" does not.

- Fed examiners focus on sustainability. They want to know the fix won't regress six months later.

- CFPB examiners are consumer-harm focused. The response must quantify affected consumers and describe remediation for each one.

- Every examiner reads the timeline first. If the dates don't make logical sense, they distrust the entire submission.

Tone calibration per regulator:

- OCC: Formal, precise, control-framework-focused. Show the structure.

- Fed: Analytical, risk-aware, forward-looking. Show the sustainability.

- CFPB: Consumer-centric, remediation-focused. Show the harm assessment and what you did about it.

- State regulators: Variable — the AI adapts based on historical patterns for each jurisdiction.

Module 4: Simulate

Purpose: Stress-test regulatory readiness by simulating a full examination before the real one arrives.

The analogy is penetration testing in cybersecurity: you hire someone to attack your systems before a real attacker does. Simulate is the compliance equivalent — an adversarial AI that attacks your regulatory posture before a real examiner can.

Agents

| Agent | Role |

|---|---|

| Examiner Persona Engine | Roleplays as a specific type of examiner — OCC safety and soundness, Fed SR 11-7 model risk, CFPB fair lending, BSA/AML. Adapts questioning style, focus areas, and depth based on examiner type and historical behavior patterns. |

| Document Reviewer | Reviews the bank's policies, procedures, and evidence as a real examiner would. Surfaces weaknesses, inconsistencies, and missing documentation. |

| Interview Simulator | Simulates examiner interviews with compliance staff. Generates the exact questions an examiner would ask, evaluates the answers, flags where staff would struggle under real examination pressure. |

| Readiness Scorer | Produces an overall examination readiness assessment by control domain, with specific improvement recommendations ranked by risk. |

Examiner Personas — What Makes This Unique

Each persona is built from observed examination behavior patterns across decades of real regulatory interactions.

The OCC Examiner: Reads every line of the control narrative. Asks "show me the evidence" for every assertion. Focuses on completeness, accuracy, and timeliness. Red flags: vague language, missing dates, unassigned owners.

The Fed Examiner: Cares about the risk framework more than individual controls. Asks "how does this connect to your enterprise risk appetite?" Focuses on model validation, stress testing, scenario analysis. Red flags: siloed controls, no escalation path, no board-level oversight.

The CFPB Examiner: Starts with the customer complaints data, always. Asks "how many consumers were affected and what did you do about it?" Focuses on fair lending, UDAAP, and complaint management. Red flags: disparate impact patterns, slow remediation timelines, incomplete complaint tracking.

The BSA/AML Examiner: Follows the money and the SARs. Asks "walk me through your transaction monitoring tuning methodology." Focuses on CDD/EDD, SAR quality, and model tuning. Red flags: low SAR rates without documented justification, no model validation, weak beneficial ownership procedures.

Module 5: Report

Purpose: Generate every report the bank needs — for the board, for the C-suite, for the regulators, for internal audit — automatically, on schedule, formatted to the audience.

Report is the module that makes the platform's value visible at the executive level. Every insight the other four modules generate flows into Report, which turns data into decisions.

Agents

| Agent | Role |

|---|---|

| Board Report Generator | Produces strategic regulatory risk summaries at the appropriate level of abstraction — strategic, not tactical. |

| Executive Brief Generator | Generates CRO/CCO-level reports with enough detail to act on but not so much that it overwhelms. |

| Regulatory Package Compiler | Assembles formal packages for regulator submission, formatted to each regulator's specific expectations. |

| Trend Analyst | Produces trend reports: "Here's how your regulatory posture has changed over the past 6, 12, and 24 months." |

| Audit Committee Reporter | Generates reports specifically for the audit committee — control effectiveness, remediation progress, examination readiness. |

Key Feature: Auto-Scheduling

Reports are generated automatically on schedule — weekly, monthly, quarterly. Stakeholders receive their version without manual compilation. Board meeting approaching? The report is pre-generated and queued for review 48 hours before the meeting.

No one should spend time compiling a status report when the data already exists. Report ensures they never have to.

Tech Stack

Frontend

- Next.js — server components, App Router, Vercel deployment

- Tailwind CSS — rapid, consistent UI development

- Recharts or Tremor — dashboards and data visualization

- React PDF — report generation

Backend

- Next.js API Routes or Node.js / Express for the API layer

- Python microservices for AI agent orchestration (LangGraph or custom multi-agent framework)

- PostgreSQL — structured data: tenants, users, findings, obligations, evidence

- Pinecone or Weaviate — vector store for document embeddings and the knowledge base

- Redis — caching, rate limiting, feature flag state

AI Layer

- Claude API (Anthropic) — core reasoning: response drafting, analysis, finding decomposition

- Custom agent orchestration — multi-agent system routing tasks to specialized agents

- RAG pipeline — documents → embeddings → vector store → context-aware generation

Infrastructure

- Vercel — frontend hosting

- AWS or Azure — backend services (banks require enterprise cloud infrastructure)

- SOC 2 compliance path — architecture choices made with this certification in mind from day one

- Terraform — infrastructure-as-code for reproducible, auditable deployments

Security (Non-Negotiable for Bank Adoption)

- Tenant data isolation at the database level — row-level security or separate schemas

- Encryption at rest (AES-256) and in transit (TLS 1.3)

- SSO/SAML integration

- Immutable audit logging on every AI action

- SOC 2 Type II certification path

- Data residency controls — US-only processing for US banks

- Penetration testing on a regular, documented schedule

Data Model

The core entity hierarchy — every object in the platform traces back to a Tenant.

Tenant (bank)

├── Users (roles, permissions)

├── Control Inventory

│ ├── Control Domain

│ ├── Control Description

│ ├── Owner

│ ├── Testing Frequency

│ └── Evidence Requirements

├── Findings

│ ├── Source (MRA, consent order, internal audit, etc.)

│ ├── Regulator (OCC, Fed, CFPB, FDIC, etc.)

│ ├── Date Received

│ ├── Status (open → in-progress → remediated → validated → closed)

│ └── Obligations[]

│ ├── Obligation Text

│ ├── Control Mapping[]

│ ├── Gap Analysis

│ ├── Remediation Plan

│ │ ├── Milestones[]

│ │ ├── Owner

│ │ ├── Evidence Checklist[]

│ │ └── Target Timeline

│ └── Response Draft

├── Documents

│ ├── Type (regulatory letter, policy, procedure, evidence)

│ ├── Embeddings (vector store reference)

│ └── Chain of Custody Log

├── Reports[]

├── Simulations[]

└── Regulatory Alerts[]

The design principle: every object in the system is traceable to a source, an owner, and a timestamp. Regulators audit. The data model is built to survive that audit.

Pricing & Monetization

Module Pricing Matrix

| Module | Tier | Annual Price Range | Primary Buyer |

|---|---|---|---|

| Monitor | Standard | $100K–$150K | Compliance Team |

| Predict | Standard | $100K–$150K | CCO / CRO |

| Defend | Premium | $200K–$400K | CCO / General Counsel |

| Simulate | Enterprise | $150K–$300K | Internal Audit / CCO |

| Report | Standard | $75K–$125K | Board Secretary / CCO |

| Full Platform | Enterprise | $500K–$1M | C-Suite |

Pricing Strategy

Land with one module at an accessible price point — likely Monitor (low urgency, easy approval) or Defend (high urgency, immediate ROI).

Expand as value is proven — turn on additional modules quarterly. The expansion conversation happens after the customer has already seen the platform deliver. It is a renewal conversation, not a sales conversation.

Full platform discount — 20–30% discount versus à la carte pricing, incentivizing the long-term commitment.

Usage-based add-on — per-document processing fees above a volume threshold, creating a natural revenue escalator as the bank's usage grows.

Go-to-Market

A solo-founder playbook, phased for capital efficiency and proof-point accumulation.

Phase 1: Build & Validate (Months 1–3)

Build the Core Engine and Defend module MVP. Recruit 2–3 design partners from the existing network — former colleagues at Tier-1 banks who have personally experienced the pain this platform solves. Run the platform on real, anonymized findings. Iterate based on what actually happens when compliance professionals use it.

Phase 2: First Revenue (Months 4–6)

Convert design partners to paying customers. Target: 2–3 banks on the Defend module. Revenue target: $400K–$800K ARR. Build the Monitor module in parallel using learnings from the design partner phase.

Phase 3: Expand (Months 7–12)

Turn Monitor on for existing customers (upsell). Build Predict and Report modules. Target: 5–8 banks across modules. Revenue target: $1M–$2M ARR. Begin the content engine: case studies, regulatory analysis, thought leadership — the exact kind of content that builds authority in the compliance community.

Phase 4: Scale (Year 2)

Full platform available. Simulate module as premium enterprise differentiator. Target: 10–15 banks. Revenue target: $3M–$5M ARR. Decision point: stay lean or make the first strategic hires.

Sales Channels

- Direct network — former colleagues across 6 Tier-1 banks. This is a relationship business.

- LinkedIn — already active, continue building authority with original content

- Conference speaking — RegTech conferences, compliance summits, ABA events

- Referrals — compliance is a small world. Happy CCOs talk to other CCOs.

- Content marketing — this platform itself, case studies, and regulatory analysis

What Makes This World-Class

Five things that cannot be replicated by any competitor starting today.

1. No one else has the training data. Examiner psychology, what response language actually passes first-pass review, which evidence documents examiners find credible versus performative — this knowledge lives in the pattern of 20 years of direct examiner-facing work. It is not available in any public dataset. It gets encoded into the agents as structured knowledge that cannot be bought or scraped.

2. No one else closes the loop. Every existing RegTech competitor does monitoring or workflow management. Archer tracks tickets. ServiceNow GRC tracks process steps. Neither predicts what's coming, drafts a response when it arrives, simulates the examiner's reaction, or generates the board report automatically. RegTwin AI does all five. End-to-end.

3. The AI doesn't just track — it thinks. It drafts regulatory response letters calibrated to the specific regulator. It simulates examination conversations with your compliance staff. It predicts which findings are coming based on peer institution patterns. This is autonomous regulatory intelligence, not a ticket tracker with a modern UI.

4. Built by a practitioner, not a startup. The buyer knows the person who built this has sat in their chair — has managed the MRA response, has presented the remediation plan to the board, has interacted directly with OCC and Fed examiners. That credibility is unchallengeable in a way that a venture-backed startup's credibility is not.

5. Modular architecture meets every customer at their current state of need. Small bank with limited budget? Start with Monitor at $100K. Bank under an active consent order? Start with Defend at $200K. Examination arriving in 90 days? Start with Simulate. Every entry point leads naturally to the full platform — and the full platform is where the real value lives.

That’s the full picture.

More from The Studio

All Papers →

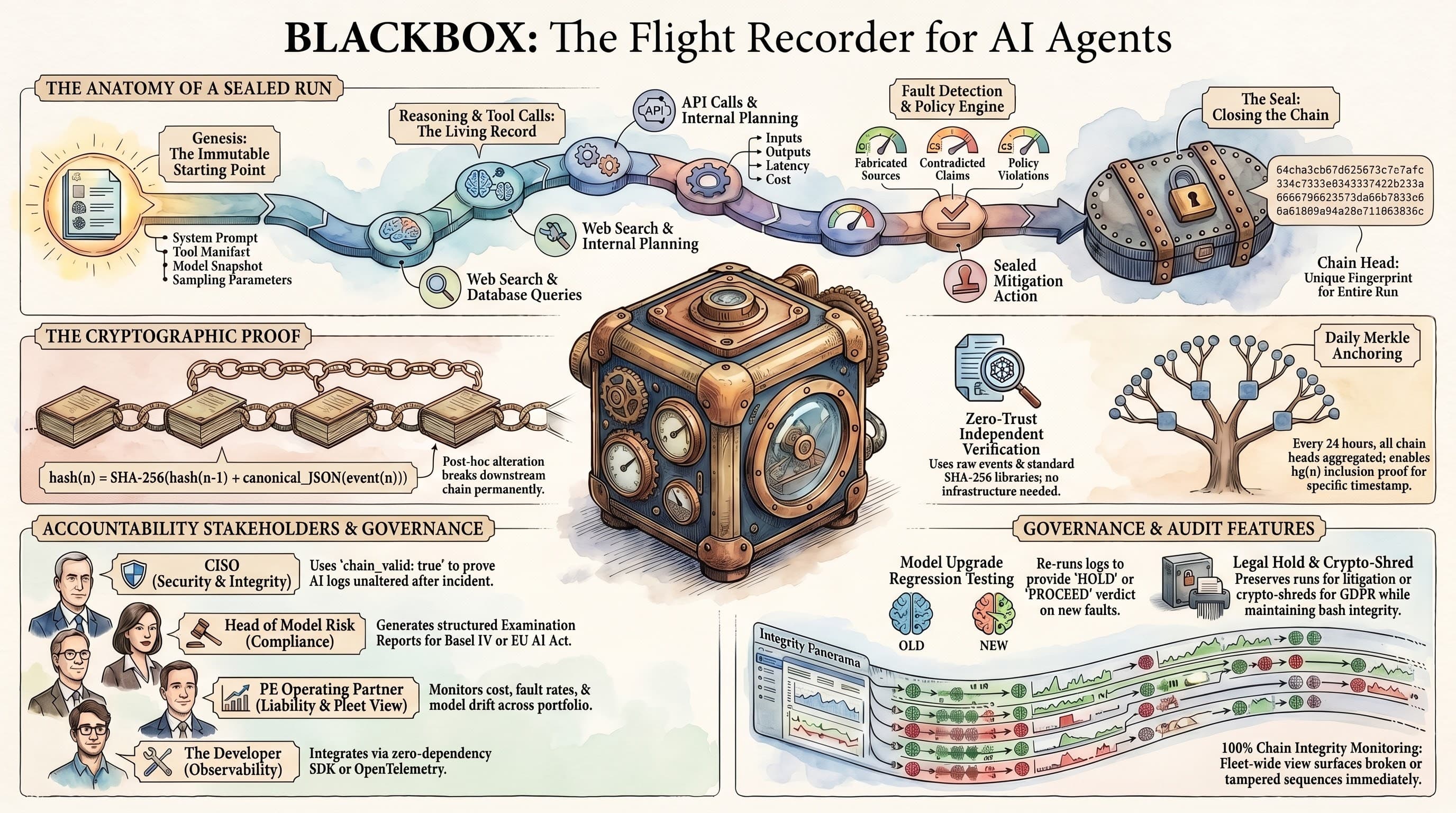

BLACKBOX: The Flight Recorder for AI Agents

When an AI agent makes a wrong decision, enterprises need to answer three questions: what exactly happened, in what order, and can the record be trusted? BLACKBOX provides the infrastructure layer that makes all three answerable. Every event — reasoning step, tool call, output, fault — is sealed into a SHA-256 hash chain. Any alteration to any stored event breaks the chain. Any run can be replayed verbatim. This paper documents the architecture, the three instrumentation paths, the phases completed, and the enterprise case for treating AI agent observability as an insurance requirement, not a nice-to-have.

The Token Economy: A First-Principles Playbook for Governing Claude in Production

At 11:47 PM on a Thursday, a Series C fintech spent its entire monthly inference budget in four hours. The root cause wasn't a malformed JSON — it was the absence of a governance discipline that should have been established before a single line of code was written. This paper specifies that discipline: four levers, one planning artifact, one role, one cadence — in the vocabulary CFOs, CTOs, and Staff+ Engineers already use.

Want to go deeper?

Discuss this paper with my digital twin.

Ask questions, challenge the framework, explore implications.

Open the Digital Twin